DC DOING BUSINESS GUIDE 2018/2019 43

ISSUES TO CONSIDER ��ADVANTAGES ��DISADVANTAGES

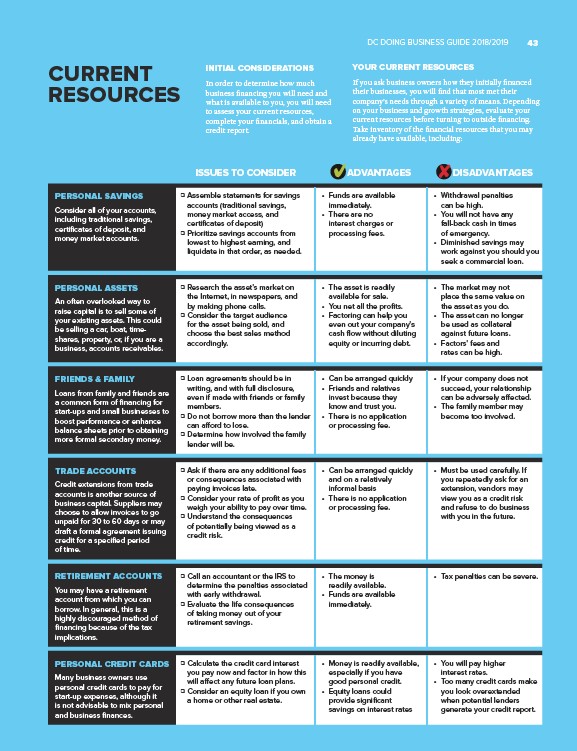

PERSONAL SAVINGS

Consider all of your accounts,

including traditional savings,

certificates of deposit, and

money market accounts.

�� Assemble statements for savings

accounts (traditional savings,

money market access, and

certificates of deposit)

�� Prioritize savings accounts from

lowest to highest earning, and

liquidate in that order, as needed.

• Funds are available

immediately.

• There are no

interest charges or

processing fees.

• Withdrawal penalties

can be high.

• You will not have any

fall-back cash in times

of emergency.

• Diminished savings may

work against you should you

seek a commercial loan.

PERSONAL ASSETS

An often overlooked way to

raise capital is to sell some of

your existing assets. This could

be selling a car, boat, timeshares,

property, or, if you are a

business, accounts receivables.

�� Research the asset’s market on

the Internet, in newspapers, and

by making phone calls.

�� Consider the target audience

for the asset being sold, and

choose the best sales method

accordingly.

• The asset is readily

available for sale.

• You net all the profits.

• Factoring can help you

even out your company’s

cash flow without diluting

equity or incurring debt.

• The market may not

place the same value on

the asset as you do.

• The asset can no longer

be used as collateral

against future loans.

• Factors’ fees and

rates can be high.

FRIENDS & FAMILY

Loans from family and friends are

a common form of financing for

start-ups and small businesses to

boost performance or enhance

balance sheets prior to obtaining

more formal secondary money.

�� Loan agreements should be in

writing, and with full disclosure,

even if made with friends or family

members.

�� Do not borrow more than the lender

can afford to lose.

�� Determine how involved the family

lender will be.

• Can be arranged quickly

• Friends and relatives

invest because they

know and trust you.

• There is no application

or processing fee.

• If your company does not

succeed, your relationship

can be adversely affected.

• The family member may

become too involved.

TRADE ACCOUNTS

Credit extensions from trade

accounts is another source of

business capital. Suppliers may

choose to allow invoices to go

unpaid for 30 to 60 days or may

draft a formal agreement issuing

credit for a specified period

of time.

�� Ask if there are any additional fees

or consequences associated with

paying invoices late.

�� Consider your rate of profit as you

weigh your ability to pay over time.

�� Understand the consequences

of potentially being viewed as a

credit risk.

• Can be arranged quickly

and on a relatively

informal basis

• There is no application

or processing fee.

• Must be used carefully. If

you repeatedly ask for an

extension, vendors may

view you as a credit risk

and refuse to do business

with you in the future.

RETIREMENT ACCOUNTS

You may have a retirement

account from which you can

borrow. In general, this is a

highly discouraged method of

financing because of the tax

implications.

�� Call an accountant or the IRS to

determine the penalties associated

with early withdrawal.

�� Evaluate the life consequences

of taking money out of your

retirement savings.

• The money is

readily available.

• Funds are available

immediately.

• Tax penalties can be severe.

PERSONAL CREDIT CARDS

Many business owners use

personal credit cards to pay for

start-up expenses, although it

is not advisable to mix personal

and business finances.

�� Calculate the credit card interest

you pay now and factor in how this

will affect any future loan plans.

�� Consider an equity loan if you own

a home or other real estate.

• Money is readily available,

especially if you have

good personal credit.

• Equity loans could

provide significant

savings on interest rates

• You will pay higher

interest rates.

• Too many credit cards make

you look overextended

when potential lenders

generate your credit report.

CURRENT

RESOURCES

INITIAL CONSIDERATIONS

In order to determine how much

business financing you will need and

what is available to you, you will need

to assess your current resources,

complete your financials, and obtain a

credit report.

YOUR CURRENT RESOURCES

If you ask business owners how they initially financed

their businesses, you will find that most met their

company’s needs through a variety of means. Depending

on your business and growth strategies, evaluate your

current resources before turning to outside financing.

Take inventory of the financial resources that you may

already have available, including: