56 ©2018 WASHINGTON DC ECONOMIC PARTNERSHIP BUSINESS TAXES

EMPLOYER TAXES

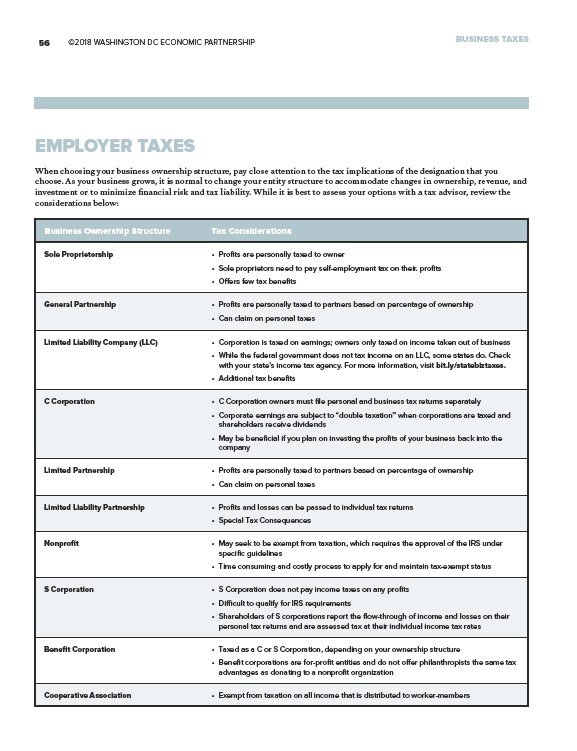

When choosing your business ownership structure, pay close attention to the tax implications of the designation that you

choose. As your business grows, it is normal to change your entity structure to accommodate changes in ownership, revenue, and

investment or to minimize financial risk and tax liability. While it is best to assess your options with a tax advisor, review the

considerations below:

Business Ownership Structure Tax Considerations

Sole Proprietorship • Profits are personally taxed to owner

• Sole proprietors need to pay self-employment tax on their. profits

• Offers few tax benefits

General Partnership • Profits are personally taxed to partners based on percentage of ownership

• Can claim on personal taxes

Limited Liability Company (LLC) • Corporation is taxed on earnings; owners only taxed on income taken out of business

• While the federal government does not tax income on an LLC, some states do. Check

with your state’s income tax agency. For more information, visit bit.ly/statebiztaxes.

• Additional tax benefits

C Corporation • C Corporation owners must file personal and business tax returns separately

• Corporate earnings are subject to “double taxation” when corporations are taxed and

shareholders receive dividends

• May be beneficial if you plan on investing the profits of your business back into the

company

Limited Partnership • Profits are personally taxed to partners based on percentage of ownership

• Can claim on personal taxes

Limited Liability Partnership • Profits and losses can be passed to individual tax returns

• Special Tax Consequences

Nonprofit • May seek to be exempt from taxation, which requires the approval of the IRS under

specific guidelines

• Time consuming and costly process to apply for and maintain tax-exempt status

S Corporation • S Corporation does not pay income taxes on any profits

• Difficult to qualify for IRS requirements

• Shareholders of S corporations report the flow-through of income and losses on their

personal tax returns and are assessed tax at their individual income tax rates

Benefit Corporation • Taxed as a C or S Corporation, depending on your ownership structure

• Benefit corporations are for-profit entities and do not offer philanthropists the same tax

advantages as donating to a nonprofit organization

Cooperative Association • Exempt from taxation on all income that is distributed to worker-members