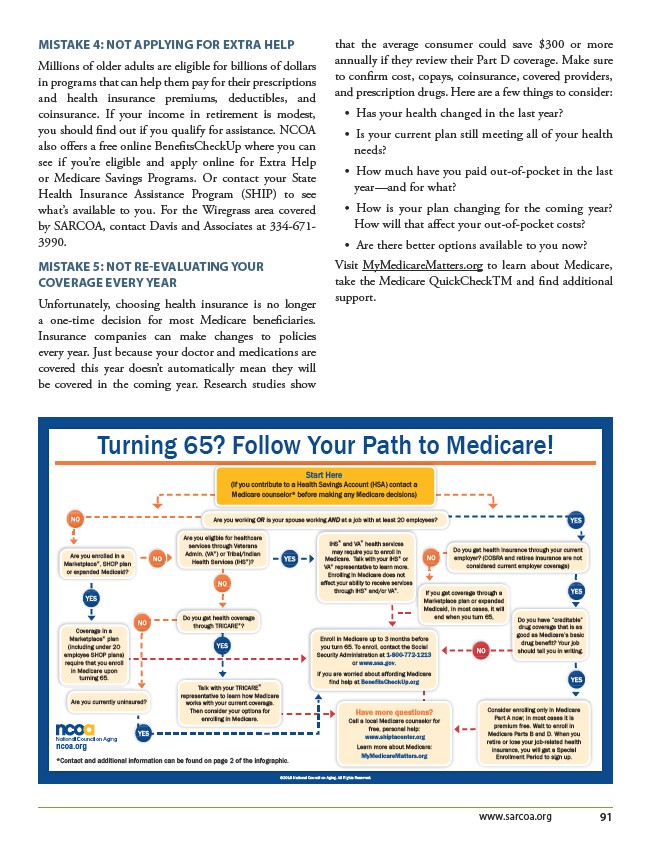

Do you get health insurance through your current

employer? (COBRA and retiree insurance are not

considered current employer coverage)

www.sarcoa.org 91

MISTAKE 4: NOT APPLYING FOR EXTRA HELP

Millions of older adults are eligible for billions of dollars

in programs that can help them pay for their prescriptions

and health insurance premiums, deductibles, and

coinsurance. If your income in retirement is modest,

you should find out if you qualify for assistance. NCOA

also offers a free online BenefitsCheckUp where you can

see if you’re eligible and apply online for Extra Help

or Medicare Savings Programs. Or contact your State

Health Insurance Assistance Program (SHIP) to see

what’s available to you. For the Wiregrass area covered

by SARCOA, contact Davis and Associates at 334-671-

3990.

MISTAKE 5: NOT RE-EVALUATING YOUR

COVERAGE EVERY YEAR

Unfortunately, choosing health insurance is no longer

a one-time decision for most Medicare beneficiaries.

Insurance companies can make changes to policies

every year. Just because your doctor and medications are

covered this year doesn’t automatically mean they will

be covered in the coming year. Research studies show

that the average consumer could save $300 or more

annually if they review their Part D coverage. Make sure

to confirm cost, copays, coinsurance, covered providers,

and prescription drugs. Here are a few things to consider:

• Has your health changed in the last year?

• Is your current plan still meeting all of your health

needs?

• How much have you paid out-of-pocket in the last

year—and for what?

• How is your plan changing for the coming year?

How will that affect your out-of-pocket costs?

• Are there better options available to you now?

Visit MyMedicareMatters.org to learn about Medicare,

take the Medicare QuickCheckTM and find additional

support.

Turning 65? Follow Your Path to Medicare!

Are you working OR is your spouse working AND at a job with at least 20 employees?

If you get coverage through a

Marketplace plan or expanded

Medicaid, in most cases, it will

end when you turn 65, Do you have “creditable”

drug coverage that is as

good as Medicare’s basic

drug benefit? Your job

should tell you in writing.

*Contact and additional information can be found on page 2 of the infographic.

©2018 National Council on Aging. All Rights Reserved.

ncoa.org

IHS* and VA* health services

may require you to enroll in

Medicare. Talk with your IHS* or

VA* representative to learn more.

Enrolling in Medicare does not

affect your ability to receive services

through IHS* and/or VA*.

Enroll in Medicare up to 3 months before

you turn 65. To enroll, contact the Social

Security Administration at 1-800-772-1213

or www.ssa.gov.

If you are worried about affording Medicare

find help at BenefitsCheckUp.org

Have more questions?

Call a local Medicare counselor for

free, personal help:

www.shiptacenter.org

Learn more about Medicare:

MyMedicareMatters.org

Consider enrolling only in Medicare

Part A now; in most cases it is

premium free. Wait to enroll in

Medicare Parts B and D. When you

retire or lose your job-related health

insurance, you will get a Special

Enrollment Period to sign up.

Are you eligible for healthcare

services through Veterans

Admin. (VA*) or Tribal/Indian

Health Services (IHS*)?

Are you enrolled in a

Marketplace*, SHOP plan

or expanded Medicaid?

Are you currently uninsured?

Do you get health coverage

through TRICARE*?

Coverage in a

Marketplace* plan

(including under 20

employee SHOP plans)

require that you enroll

in Medicare upon

turning 65.

Start Here

(If you contribute to a Health Savings Account (HSA) contact a

Medicare counselor* before making any Medicare decisions)

Talk with your TRICARE*

representative to learn how Medicare

works with your current coverage.

Then consider your options for

enrolling in Medicare.

/www.ssa.gov

/www.sarcoa.org

/MyMedicareMatters.org

/MyMedicareMatters.org

/ncoa.org

/www.ssa.gov

/BenefitsCheckUp.org

/www.shiptacenter.org