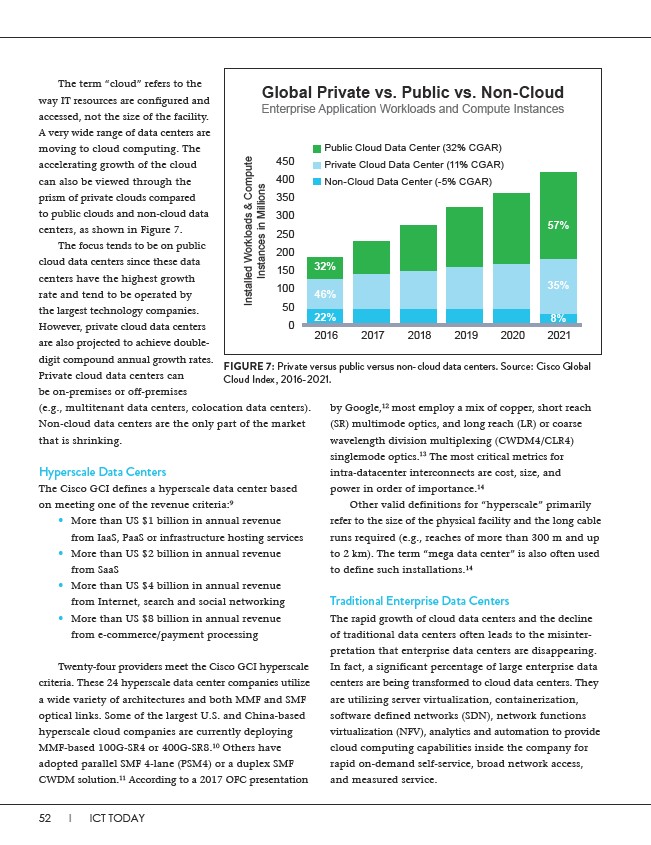

The term “cloud” refers to the

way IT resources are configured and

accessed, not the size of the facility.

A very wide range of data centers are

moving to cloud computing. The

accelerating growth of the cloud

can also be viewed through the

prism of private clouds compared

to public clouds and non-cloud data

centers, as shown in Figure 7.

The focus tends to be on public

cloud data centers since these data

centers have the highest growth

rate and tend to be operated by

the largest technology companies.

However, private cloud data centers

are also projected to achieve doubledigit

compound annual growth rates.

Private cloud data centers can

be on-premises or off-premises

52 I ICT TODAY

Global Private vs. Public vs. Non-Cloud

Enterprise Application Workloads and Compute Instances

by Google,12 most employ a mix of copper, short reach

(SR) multimode optics, and long reach (LR) or coarse

wavelength division multiplexing (CWDM4/CLR4)

singlemode optics.13 The most critical metrics for

intra-datacenter interconnects are cost, size, and

power in order of importance.14

Other valid definitions for “hyperscale” primarily

refer to the size of the physical facility and the long cable

runs required (e.g., reaches of more than 300 m and up

to 2 km). The term “mega data center” is also often used

to define such installations.14

Traditional Enterprise Data Centers

The rapid growth of cloud data centers and the decline

of traditional data centers often leads to the misinterpretation

that enterprise data centers are disappearing.

In fact, a significant percentage of large enterprise data

centers are being transformed to cloud data centers. They

are utilizing server virtualization, containerization,

software defined networks (SDN), network functions

virtualization (NFV), analytics and automation to provide

cloud computing capabilities inside the company for

rapid on-demand self-service, broad network access,

and measured service.

450

400

350

300

250

200

150

100

50

(e.g., multitenant data centers, colocation data centers).

Non-cloud data centers are the only part of the market

that is shrinking.

Hyperscale Data Centers

The Cisco GCI defines a hyperscale data center based

on meeting one of the revenue criteria:9

• More than US $1 billion in annual revenue

from IaaS, PaaS or infrastructure hosting services

• More than US $2 billion in annual revenue

from SaaS

• More than US $4 billion in annual revenue

from Internet, search and social networking

• More than US $8 billion in annual revenue

from e-commerce/payment processing

Twenty-four providers meet the Cisco GCI hyperscale

criteria. These 24 hyperscale data center companies utilize

a wide variety of architectures and both MMF and SMF

optical links. Some of the largest U.S. and China-based

hyperscale cloud companies are currently deploying

MMF-based 100G-SR4 or 400G-SR8.10 Others have

adopted parallel SMF 4-lane (PSM4) or a duplex SMF

CWDM solution.11 According to a 2017 OFC presentation

2016

0

2017 2018 2019 2020 2021

Installed Workloads & Compute

Instances in Millions

Public Cloud Data Center (32% CGAR)

Private Cloud Data Center (11% CGAR)

Non-Cloud Data Center (-5% CGAR)

57%

32%

46%

22%

35%

8%

FIGURE 7: Private versus public versus non-cloud data centers. Source: Cisco Global

Cloud Index, 2016-2021.